The impact of the FCA rules on the payday loan industry

In 2015 the Financial Conduct Authority (FCA) introduced stricter rules on payday lending to help regulate the market, making it fairer for borrowers. Our latest report looks at differences in the industry since these changes were brought in.

The new rules included:

- A price cap on high cost short-term credit (HCSTC)

- Limits on how many times a payday loan could roll over

- Stronger guidance on affordability checks and financial health warnings

To develop an insight in to the impact these changes had, we compared clients with HCSTC debts who came to us in the first half of 2013 with clients with HCSTC debts who came to us in the first half of 2016. We also surveyed clients with HCSTC debts who had applied for a payday loan since the introduction of the stricter rules.

How the payday loans market has changed?

Our findings show that although there are some welcome signs of improvement, the HCSTC market has changed and adapted to a new, post price cap industry.

An example of these changes includes the introduction of instalment loans, typically between 3-6 months. Rather than the (intended) one month repayment period that was typical of payday loans. Meaning that although repayments may be lower and more manageable, there’s more time for interest to build up making them more expensive overall.

Our evidence suggests that:

- Some borrowers still don’t fully understand how much they have to repay on a loan

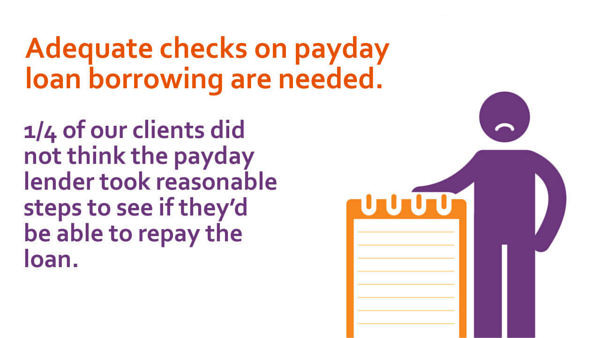

- Some don’t think the HCSTC lender took reasonable steps to see if they’d be able to repay the loan

- Worryingly, some people could still take out high-cost short-term credit loans when they already had considerable other debts, including other HCSTC debts

- A third of clients with HCSTC have three or more of these debts

It’s clear that poor practice is still evident in the payday loan industry. We’re urging the FCA to look closer at responsible lending measures in the HCSTC market.

Other key findings from the report include:

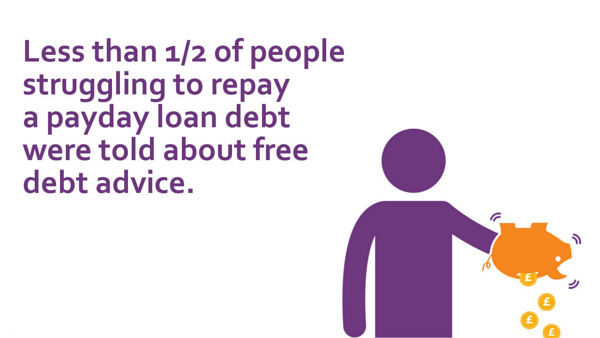

- After telling the lender they were struggling to repay, less than half of our clients were told about free debt advice

- Just under a quarter of clients found the lender continued to demand payment even when they were told about the client’s financial difficulties. One in ten of those were threatened with court or other enforcement action

- Despite the stricter regulations on payday loans and the expansion of credit unions, there’s still a need for greater affordable credit alternatives

Many clients told us about the impossible choices they face between taking out high cost credit, missing a household bill payment or not having enough money to pay for essentials like feeding their family.

Our six recommendations to help improve the HCSTC market

Our report calls for more to be done to make this type of lending better for borrowers, and investigates what alternative forms of more affordable credit are needed for those that are more financially vulnerable.

The key recommendations are:

1. The FCA should explore, as part of their review of the price cap, what the implications of the shift to instalment loans are for the appropriate level of the price cap.

2. The FCA should strengthen their rules on responsible lending, including turning their existing guidance on responsible lending into rules. For example, creditworthiness assessments should be required to take account of whether the customer is experiencing difficulties with their existing financial commitments.

3. The FCA price cap review should have a broad scope to include the continuing issues with the treatment of customers in arrears and how to tackle them.

4. HCSTC lenders should ensure that their debt collection practices are based on supporting affordable and sustainable repayments and providing appropriate support to help customers in financial difficulties.

5. The FCA should ensure consistency of regulation across different forms of high cost and mainstream credit to deal with the problems financially vulnerable consumers’ experience. This would include, for example, setting a cap on unarranged overdraft charges.

6. The government needs to look at new ways to provide greater access to more affordable credit safety nets for the most financially vulnerable, including looking at international examples of no and low interest loan schemes.

Download the report now for the full picture.

Download now