Why working families fall into problem debt. Our new research

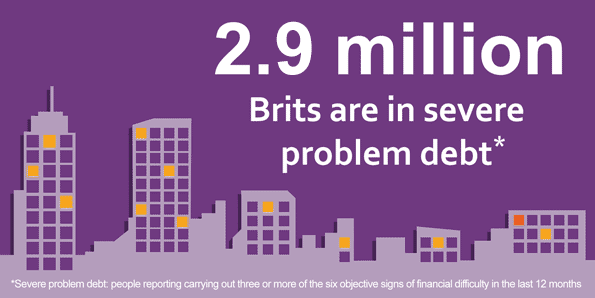

Despite a steady economic recovery and low headline unemployment, 2.9 million people are in severe problem debt and 8.8 million people are in moderate financial difficulty. Income shocks are tipping millions of people into problem debt because millions of families don’t have safety nets they can rely on.

Our research shows that 14 million people faced a shock to their income or a change of circumstance in the last year and that:

- 1.26 million people work part time because they can’t get a full time job

- 565,000 work a temporary job because they can’t get a permanent job

- 790,000 people work a zero hour contract as their main job

There is still a lot of churn in the job market and people working insecure jobs through a lack of choice. This results in a ‘new normal’ of insecurity and income shocks that people need help to adjust to. People in insecure work are twice as likely to face an income shock as those with a permanent job.

Relying on credit to cope

Many people struggle to cope with income shocks on their savings and welfare. Some 6.5 million people relied on credit as part of their coping strategy – many of them found that their savings and welfare weren't enough to keep up:

- 34% of people who relied on credit couldn’t last a week on their savings

- 61% of people in problem debt receiving Jobseekers’ Allowance after a £500+ drop in their income couldn’t afford their essential costs

Relying on credit as a coping strategy tips 68% of people into financial difficulty. People who have to rely on credit to keep up with their costs after an income shock are twenty times more likely to fall into severe problem debt.

Safety nets for the realities of modern working life

Working people need safety nets that respond to the realities of modern working life, helping them bounce back quickly avoid longer term financial difficulty. But policy action on welfare has been focused on getting the long term unemployed back into the job market.

To reduce the £8.3 billion cost of problem debt, the Government needs to put in place a long term plan to boost British families’ financial resilience. Work and growth alone are not enough to keep families out of financial difficulty.

This should include action to help low income families save for a rainy day, and introduce a Breathing Space protection to help families control their credit commitments and stop them spiralling out of control.

Policymakers will also need to consider how to help people plug the gap between their income and essential costs after they’ve faced a shock to their income, so that they don’t have to turn to credit and put themselves at further risk. This is a big question, and StepChange Debt Charity will be working with policymakers over the coming year to look at realistic options for helping families cope with life’s ups and downs without relying on credit.

Download the report now for the full picture.

Download now