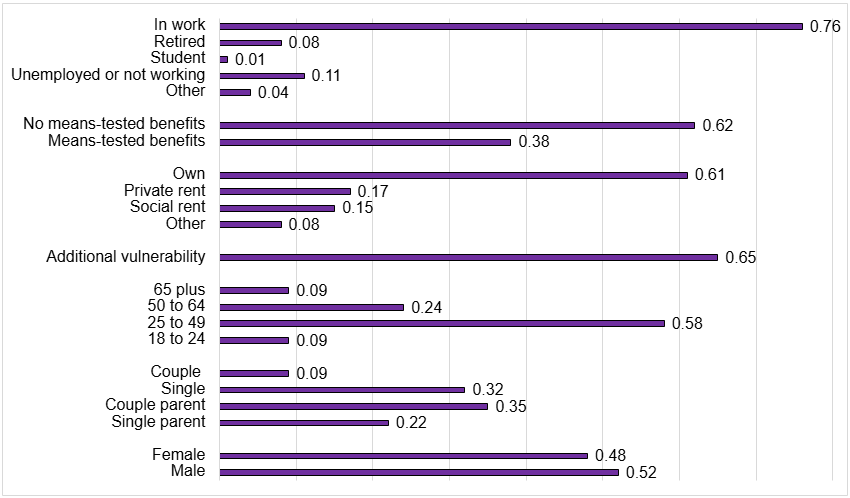

Fig. 1: Respondents with coerced debts disaggregated by benefit status, housing tenure, work status, gender and additional vulnerability

The chart shows how our sample of adults who have experienced coerced debt was split by demographic status.

The data indicated that respondents experiencing coerced debts differed from the risk factors for domestic abuse more broadly,viii where people in vulnerable circumstances are at greater risk of harm. Among the respondents, coerced debt, while creating more severe impacts for people with additional vulnerabilities, which we go on to discuss later, appeared also to be driven by opportunity (where people have stable incomes, assets and creditworthiness), with people in full-time work, homeowners, and those with a higher income no less vulnerable to coerced debt. This may also help to explain why men seem to be as commonly affected as women in our sample.

While men and those who are financially stable experienced coerced debt, those with lower incomes were disproportionately affected, with single parents, those with children under 18 and those on means-tested benefits over-represented, which reflects wider evidence of risk factors for abuse (being female, poverty, receiving benefits).

Dependence also appears to be a factor; respondents who rely on others to help them manage their life or their money experienced coerced debt in greater numbers, which again demonstrates how opportunistic perpetrators take advantage of having greater access to a victim-survivor’s finances. This is also in keeping with evidence that people with additional vulnerabilities are more susceptible to abuse,ix as well as the abuse creating more severe effects for people with additional vulnerabilities.

Overall, the data did not reveal a strong gender split. In fact, slightly more men (52%) than women (48%) indicated that they had experienced coerced debt. Given other data we have around domestic abuse, where women are disproportionately represented among victim-survivors,x it is likely that this lack of gender divide is explained by the small sample size as well as the proportion of people who experienced coercive and controlling behaviour by a family member in our survey. Wider evidence shows that domestic abuse from non-intimate partners does not come with the same gender differences as intimate partner abuse.xi Indeed, experiences of coercive and controlling behaviour were much higher among male respondents (57%) than female respondents (33%).

Wider evidence shows that some groups like those with disabilities and Black, Asian and racially minoritised people all appear more likely to experience abuse.xii 80% of the sample identified as white British and 19% as a non-white British ethnicity, but we aren’t able to draw conclusions on prevalence and how this maps onto wider trends from our data.